FHA Loan Requirements 2023

FHA Loan Requirements 2023

FHA Loan Requirements 2023

FHA Loan Requirements 2023FHA Loan Requirements 2023

FHA announced a set of policy changes

to strengthen the FHA. The changes announced are the latest in a series

of changes enacted in order to better position the FHA to manage its

risk while continuing to support the nation’s housing market recovery.

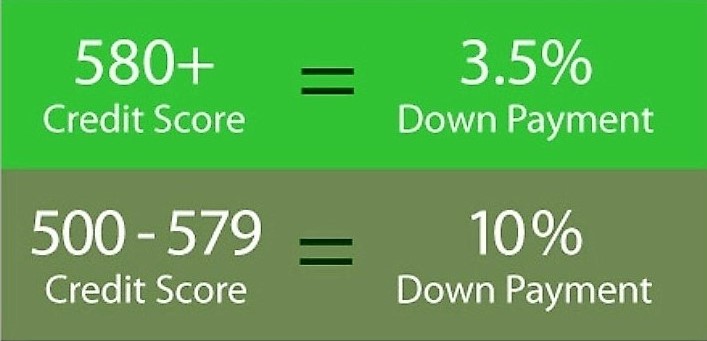

The FHA has updated the combination of credit score and down payments for new borrowers:

- 580 credit score to qualify for FHA's 3.5% down payment

- Below 580 credit score 10% down payment

- 500 minimum credit score

- No credit scores are allowed

FHA minimum credit score needed to buy a house is 500.

FHA after bankruptcy - First and foremost lenders will want to see that you have re-established your credit after the bankruptcy. Make sure that you do not miss any payments. If you are buying a home or refinancing, make sure you can provide the bankruptcy discharge paperwork.

Chapter 7

At least two years must have elapsed since the discharge date of the borrower and / or spouse's Chapter 7 Bankruptcy, according to FHA guidelines. This is not to be confused with the bankruptcy filing date. A full explanation will be required with the loan application. In order to qualify for an FHA loan, the borrower must qualify financially, have re-established credit and have a minimum 500 credit score.

Chapter 13

FHA will consider approving a borrower who is still paying on a Chapter 13 Bankruptcy if those payments have been satisfactorily made and verified for a period of one year. The court trustee's written approval will also be needed in order to proceed with the loan. The borrower will have to give a full explanation of the bankruptcy with the loan application and must also have re-established good credit, qualify financially and have good job stability.

No credit history

Three lines of credit are necessary to apply for an FHA loan. However, in the event a borrower does not have sufficient credit on their credit report the FHA will allow substitute forms. FHA allows minimum alternative trade lines if you have no credit scores.

Late payments

During an underwriter analysis of borrower credit, the overall pattern of credit behavior is being reviewed rather than isolated cases of slow payments. If a good payment pattern has been maintained, regardless of a specific period of financial difficulty preceded it, the borrower may escape disqualification.

Collection accounts

FHA does not require collection accounts to be paid off as a condition of mortgage approval. However, FHA does recognize that collection efforts by the creditor for unpaid collections could affect the borrower’s ability to repay the mortgage.

- If evidence of a payment arrangement is not available, the lender must calculate the monthly payment using 5% of the outstanding balance of each collection and include the monthly payment in the borrower’s debt-to-income ratio.

- FHA credit score needed to buy a house

FHA after foreclosure - A borrower whose previous residence or other real property was foreclosed on or has given a deed-in-lieu of foreclosure within the previous three years is generally not eligible.

Foreclosure must have been resolved for at least 3 years with no late payments since the date of resolution.

Seasoning requirements

- Government loan: Seasoning is determined by the date the claim was paid

- Loans other than Government: Seasoning is determined by the date of sale the lender sold the property

Short Sale - To be eligible for an FHA loan 3 years must have passed from the date of sale. If your mortgage payments were in default at the time of the short sale FHA requires you to wait 3 years before you can qualify for a new loan.

Debt to income ratio to buy a house

Debt to income ratios are the calculations underwriters use to determine whether a borrower can qualify for a mortgage. They are used to determine if you have the capacity to repay your mortgage.

- FHA DTI ratio is 45%/55% with credit score above 620

- FHA DTI ratio is 31%/43% with credit score below 620

There are two calculations. The first or Front Ratio is your housing expense-to-income ratio. This is your proposed mortgage payment (principle, interest, taxes, mortgage insurance, and homeowners' insurance) divided by your gross monthly income.

The second or Back Ratio is your total monthly obligations-to-income ratio. This is your gross monthly payment including Mortgage PITI divided by your gross monthly income.

FHA loans include a maximum debt to income ratio. When a borrower applies for a mortgage, they are required to disclose all debts, open lines of credit, and all possible approved sources of regular income. Using this data, the lender calculates the borrower's debt-to-income ratio.

FHA Loan Requirements 2023

FHA purchase FHA refinance FHA 203k loan FHA cash out $100 down loan

FHA loan requirements - FHA loan limits - FHA loans - FHA Streamline

Call us 800.516.9166

www.MORTGAGE-WORLD.com LLC is an online mortgage company specializing in FHA loans for first time home buyers.

We look forward to working with you.

Call us 888-958-5382

www.MORTGAGE-WORLD.com LLC is an online mortgage company specializing in FHA loans for first time home buyers.

We look forward to working with you.

Call 800.516.9166

Recent Articles

-

Cash Out Refinance Florida: Ways to Unlock Your Home Equity Fast

Mar 25, 26 04:46 PM

Discover how cash out refinance florida works, including benefits, requirements, and expert tips to access your home equity quickly and safely.

Discover how cash out refinance florida works, including benefits, requirements, and expert tips to access your home equity quickly and safely. -

Mortgage Rates August 5

Aug 05, 24 04:10 PM

Mortgage Rates August 5, 2024. Rates have gone down recently. Lower rates equals lower mortgage payment. -

Mortgage Rates August 5 2024

Aug 05, 24 03:55 PM

Mortgage Rates August 5 2024

Mortgage Rates August 5 2024

Recent Articles

-

Cash Out Refinance Florida: Ways to Unlock Your Home Equity Fast

Mar 25, 26 04:46 PM

Discover how cash out refinance florida works, including benefits, requirements, and expert tips to access your home equity quickly and safely. -

Mortgage Rates August 5

Aug 05, 24 04:10 PM

Mortgage Rates August 5, 2024. Rates have gone down recently. Lower rates equals lower mortgage payment. -

Mortgage Rates August 5 2024

Aug 05, 24 03:55 PM

Mortgage Rates August 5 2024

Call Now, Our Staff is Available!

888.958.5382